[et_pb_section fb_built=”1″ admin_label=”section” _builder_version=”3.0.47″][et_pb_row _builder_version=”3.0.47″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”][et_pb_column type=”4_4″ _builder_version=”3.0.47″ parallax=”off” parallax_method=”on”][et_pb_post_title author=”off” comments=”off” _builder_version=”3.0.47″ title_font_size=”50px” title_text_color=”#0c71c3″][/et_pb_post_title][/et_pb_column][/et_pb_row][et_pb_row admin_label=”row” _builder_version=”3.0.47″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”][et_pb_column type=”1_2″ _builder_version=”3.0.47″ parallax=”off” parallax_method=”on”][et_pb_text _builder_version=”3.0.47″ text_font_size=”30″ text_text_color=”#ffffff” header_line_height=”1.5em” background_size=”initial” background_position=”top_left” background_repeat=”repeat”]

There is risk involved but now might be a good time to invest in Johannesburg

[/et_pb_text][/et_pb_column][et_pb_column type=”1_2″ _builder_version=”3.0.47″ parallax=”off” parallax_method=”on”][et_pb_text _builder_version=”3.0.47″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”]

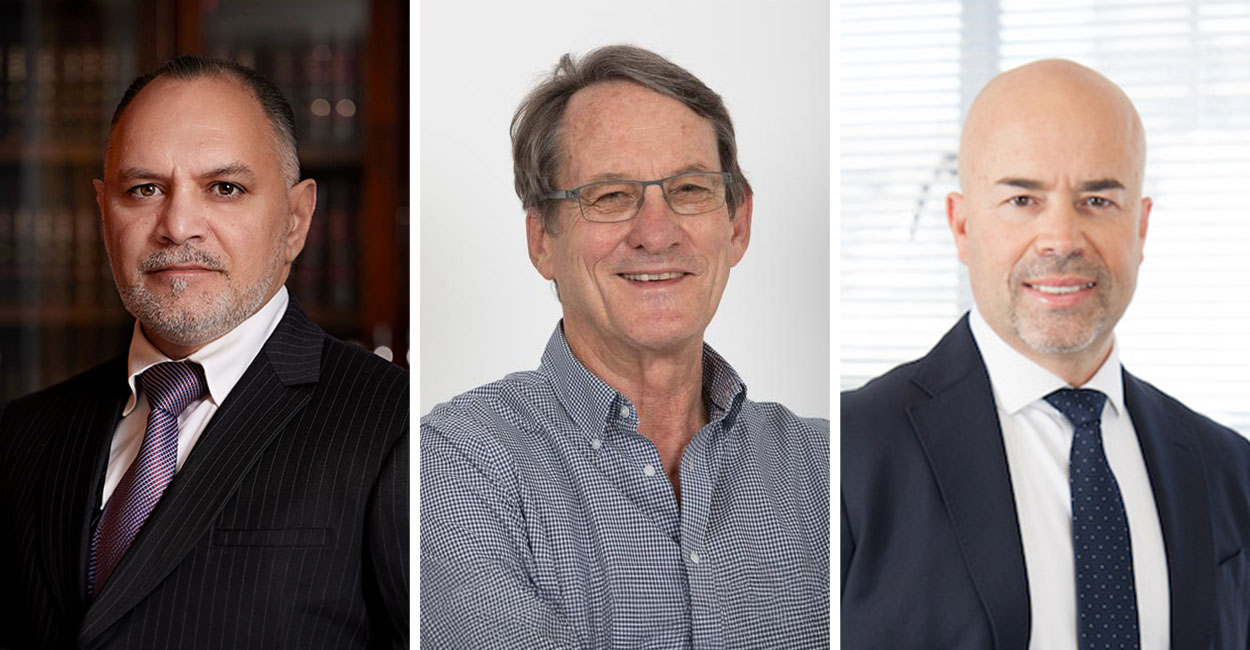

Local estate agents remain optimistic price growth in Johannesburg despite concerns about South Africa’s recent downgrade to sub-investment grade, or junk status, by major ratings agencies. Says Ronald Ennik, founder and principal of Ennik Estates: “The Johannesburg residential property market is set for an upturn after a long period of uncertainty and flat-lining prices.

[/et_pb_text][/et_pb_column][/et_pb_row][et_pb_row admin_label=”row” _builder_version=”3.0.47″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”][et_pb_column type=”4_4″ _builder_version=”3.0.47″ parallax=”off” parallax_method=”on”][et_pb_text _builder_version=”3.0.47″ text_font=”Roboto|on|||” background_size=”initial” background_position=”top_left” background_repeat=”repeat”]

Fundamentally, Johannesburg home prices at present are the most undervalued they have been in the past 20 years. There are opportunities galore to buy at discount.” He says this is because, unlike Cape Town, the Johannesburg residential property market is nowhere near topping out from a boom period – as was the case in 2007. At the same time, while the cabinet reshuffle and dismissal of Pravin Gordhan and Mcebisi Jonas as finance and deputy finance ministers respectively have caused the country to slide into junk status, Ennik says at least buyers now know what they are dealing with. “These unfortunate developments … have lifted the mantle of uncertainty that has been hanging over the property market for some time,” he says. “Buyers and sellers can at least see the lie of the land – albeit a pretty daunting picture right now.”

FILTERING DOWN

Chairman of Seeff Properties Samuel Seeff says the markets had already factored in some of these events. “The credit downgrades were expected to some extent, given that the threat has been with us for about 18 months and the effects have in many respects been factored into trading conditions.” While there will no doubt be financial consequences, these effects will only filter through much later, he says. “For now, it remains business as usual for the property market.” Candice Andrews, head offi ce branch manager for Adrienne Hersch Properties, says that while the “boom market” of years gone by is a thing of the past, even in the current “slow market” there is an enormous amount of investment and development taking place in and around Johannesburg’s northern suburbs. “As with any market, high demand is directly linked to price growth, and with weakened over the property market for some time,” he says. “Buyers and sellers can at least see the lie of the land – albeit a pretty daunting picture right now.”

DECLINING SALES?

Justine Roux, area specialist for Lew Geffen Sotheby’s International Realty, points out that house sales volumes have slowed notably in upmarket Johannesburg suburbs such as Inanda. According to Lightstone, only 10 properties with a combined value of R79.8m changed hands in Inanda in the 12 months ending 30 April, with Atholl’s 24 sales realising R146.5m. But Roux attributes the slowdown to “many more potential sales” that fell through and a lack of urgency from these sellers, as well as prices not dropping in the past two years. “One of the main reasons homes aren’t selling is that sellers simply won’t budge from their listing prices despite the notable decline in investor numbers that has precipitated a shift to a buyers’ market,” says Roux. “Many sellers in suburbs such as Inanda, Illovo and Atholl have high expectations and low financial stress, which means they can often aff ord to sit out the tight economic conditions and wait for the market to improve – however long that takes.”

“If sellers don’t come to the party on their price, buyers will simply go next door” – Candice Andrews, head office branch manager, Adrienne Hersch Properties

[/et_pb_text][/et_pb_column][/et_pb_row][et_pb_row admin_label=”row” _builder_version=”3.0.47″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”][et_pb_column type=”4_4″ _builder_version=”3.0.47″ parallax=”off” parallax_method=”on”][et_pb_text _builder_version=”3.0.47″ text_font=”Roboto|on|||” background_size=”initial” background_position=”top_left” background_repeat=”repeat”]

Cape vulnerability

While Johannesburg certainly presents opportunities, Ennik says the same cannot be said for Cape Town. “Cape Town is in a far more vulnerable situation than Johannesburg. It has been in an opposite cycle and is now ripe to come off its boom. By contrast, there is no fat in the undervalued Johannesburg market – and there is therefore less risk and more potential.” Seeff agrees that Johannesburg off ers great potential. “In terms of the Joburg property market, there is most certainly still excellent value to be had. Property prices have grown at fairly conservative rates and buyers are able to find excellent value across the market. The banks are also still lending, so it remains a good time to buy and sell – if you are a serious seller.” For these reasons, Ennik says buyers in Joburg who find the home that suits their needs and lifestyle should climb aboard now, while interest rates are still relatively low. “However, they must be aware that the rates will inevitably rise in the future.”

CAUTION PLEASE

In light of this, Seeff says all property buyers anywhere in South Africa should buy below their means and build in some room to absorb potential interest rate rises and cost increases. For sellers, market-related pricing will become increasingly important across the country. “In terms of the bulk of activity, the middle to lower sector of the market, predominantly in the R1.1m-R1.2m price band and bonds in the R900,000 to R1m range, seem to be least aff ected by the economic slow-down, with activity continuing,” Seeff says. “In contrast, the R5m-plus range is seeing a dip in activity, with buyers and investors more hesitant.” Timothy Akinnusi, executive head of home loan sales and client value management at Nedbank, says that because Gauteng is the most economically active metro in South Africa, the demand for residential property in the price range of R600,000 to R1.5m will be much stronger as the population of younger people migrate to the region for employment opportunities. “This, in turn, drives demand for new entrants into the housing market,” he says. “In the Western Cape, the demand for housing in the R4m to R8m bracket is likely to be more attractive than in Gauteng, given the demographic of holiday makers and investment property opportunities.” Ennik says the market opportunity in Johannesburg will benefit first-time buyers the most because they do not need to sell a home to buy one. “Be courageous and take the plunge because nothing ventured is nothing gained.”

“The Johannesburg residential property market is set for an upturn after a long period of uncertainty and flatlining prices” – Ronald Ennik, founder and principal, Ennik Estates

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]