BetterBond Property Brief

South Africa’s residential property market has entered 2026 with a confidence not seen since before the interest-rate surge of 2023. The latest BetterBond Property Brief paints a picture of a market in genuine recovery: record purchase prices, falling deposit requirements, and improving loan approval rates across almost every region. The catch? A war in the Middle East is threatening to undo much of the progress made.

The conflict involving Iran and the United States has closed the Strait of Hormuz, spiked Brent crude prices, and sent emerging-market currencies, including the Rand, into retreat. Investors fleeing to US Treasuries have punished assets like South African bonds, and the knock-on effects on inflation and the Reserve Bank’s rate-cutting cycle are already being felt.

“While early indicators in the property market are encouraging, ongoing global uncertainty reminds us that confidence and affordability remain closely tied to the broader economic environment,” says Stephan Potgieter, CEO of BetterHome Group Mortgage Origination and BetterBond.

The month in numbers

- 1.6% – National Treasury’s 2026 GDP growth forecast

- R3 million – new exclusion from capital gains tax on residences

- 285 basis points – decline in the 10-year bond yield (4 April 2025 to 5 March 2026)

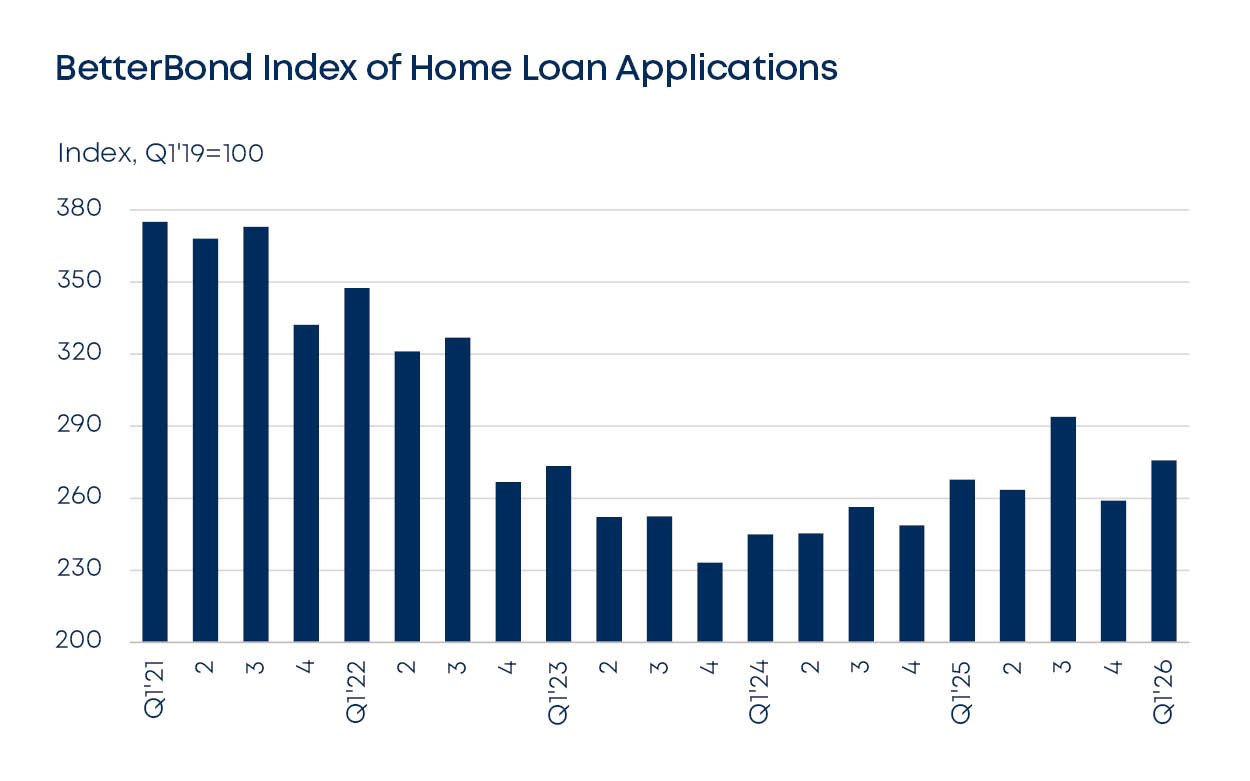

Bond applications: a market climbing back

The BetterBond Index of Home Loan Applications posted a 6.4% quarter-on-quarter increase in the first two months of 2026. More meaningfully, the year-on-year growth came in at 3% – a figure that reflects sustained recovery from the recession triggered by record-high interest rates in 2023 and 2024. Since bottoming out in Q4 2023, applications have risen a cumulative 18.2%, though they remain below the highs recorded in Q3 2021.

The prime lending rate has fallen 150 basis points since September 2024, providing meaningful relief to borrowers. However, the Reserve Bank’s Monetary Policy Committee paused its cutting cycle at the January 2026 meeting, and the geopolitical situation in the Middle East has clouded the prospect of a March reduction.

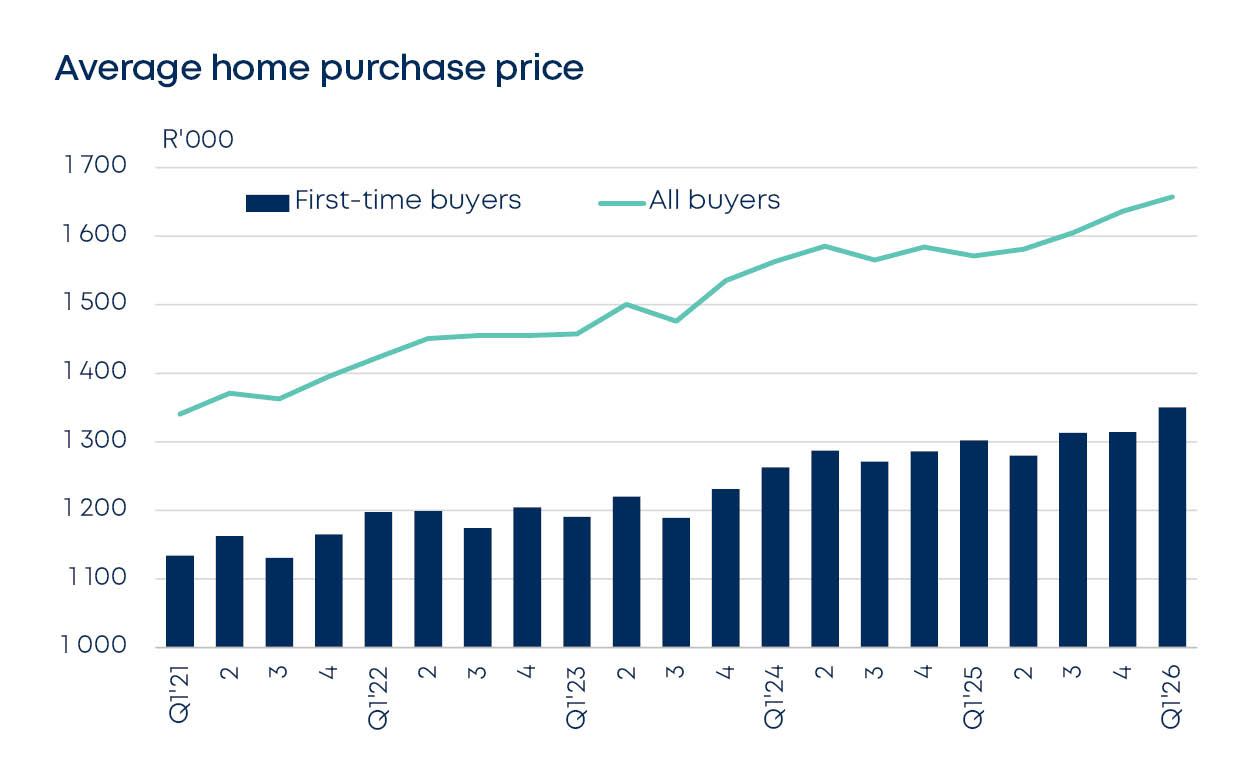

House prices: record territory for all buyers

During the first two months of 2026, average house prices reached a milestone, with positive real increases recorded for both first-time buyers (FTBs) and repeat buyers through BetterBond’s origination services. This marks the first such occurrence since before Q4 2024, in response to lower interest rates. When adjusted for inflation, the YoY increases in average house prices for all buyers and for FTBs amounted to 1.9% and 0.2%, respectively during the first two months of Q1 2026. In nominal terms, new record highs were recorded during January and February, namely R1.66 million for all buyers and R1.35 million for FTBs.

Unfortunately, the monetary policy authorities paused the rate-cutting cycle in their January meeting. Speculation has been rife that a further rate cut would occur in March, but the war in the Middle East may prevent this, due to the double-edged inflationary effect of higher oil prices and the rand’s depreciation. Hopefully, the hostilities will end sooner rather than later.

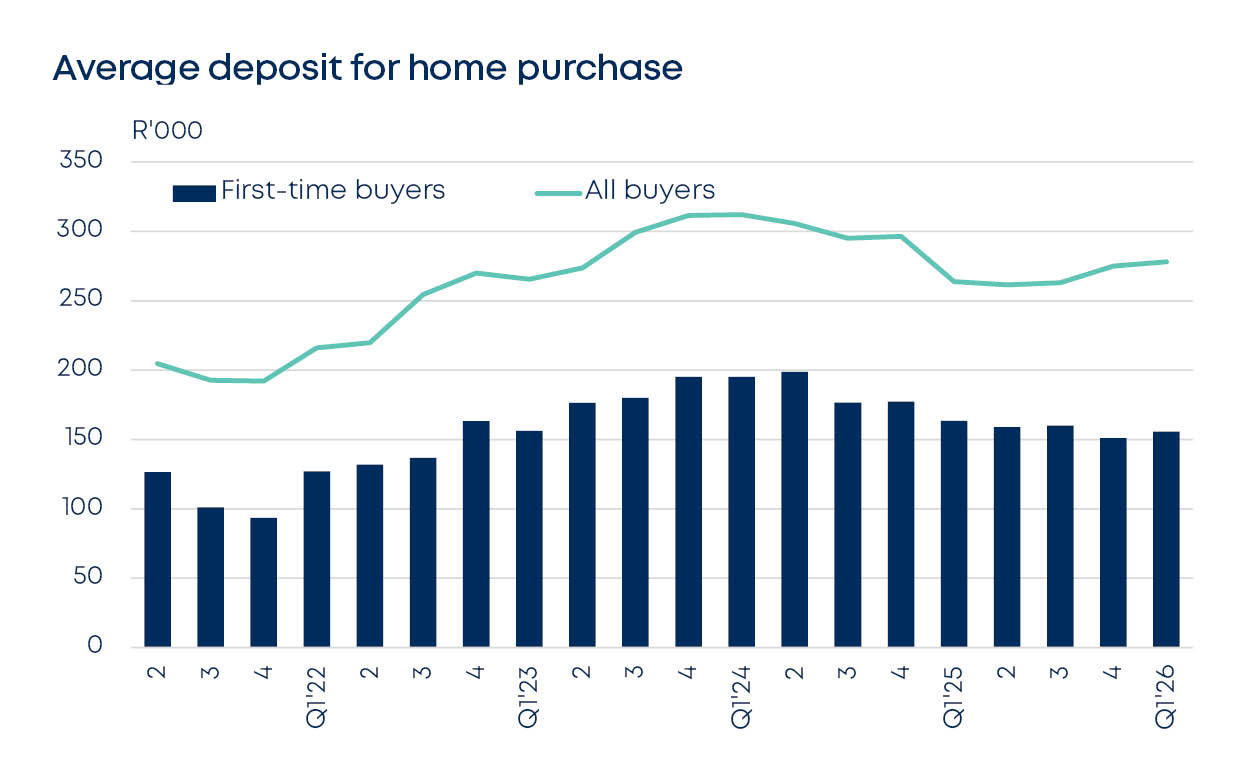

Deposits: lower than two years ago, but stalling

Deposit requirements for home loans fell steadily after peaking in early 2024, but have recently stalled — likely due to the Reserve Bank’s pause in its rate-cutting cycle. During Q1, the average deposit requirement for first-time buyers increased by 3.1% to R156,000, though this remains marginally lower than a year ago. For all buyers, the deposit requirement was virtually unchanged quarter-on-quarter at R278,000.

Compared to Q1 2024, however, the picture is meaningfully better. Deposit requirements for first-time buyers are currently 20% lower than two years ago, and 11% lower for all buyers — a structural improvement in affordability that remains intact despite the recent pause.

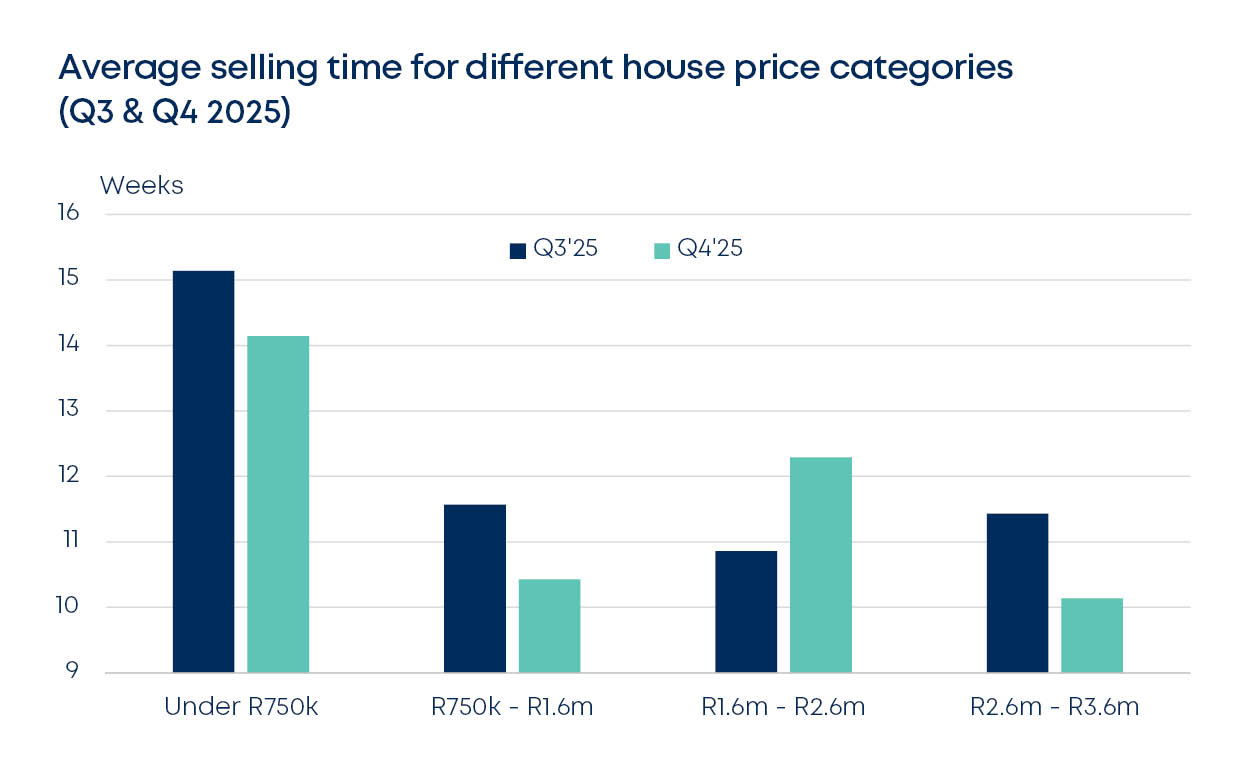

Selling times: speed depends on price and province

The Western Cape continues to lead on selling speed, with an average time on market of just six weeks and two days in Q4 2025. KwaZulu-Natal was in second place at nine weeks and four days, while Gauteng lagged at just under 14 weeks. In terms of price bracket, homes in the R2.6 million to R3.6 million range sold fastest, averaging 10 weeks and 1 day, while the R1.6 million to R2.6 million bracket proved the most challenging, with selling times edging up to 12 weeks and 2 days.

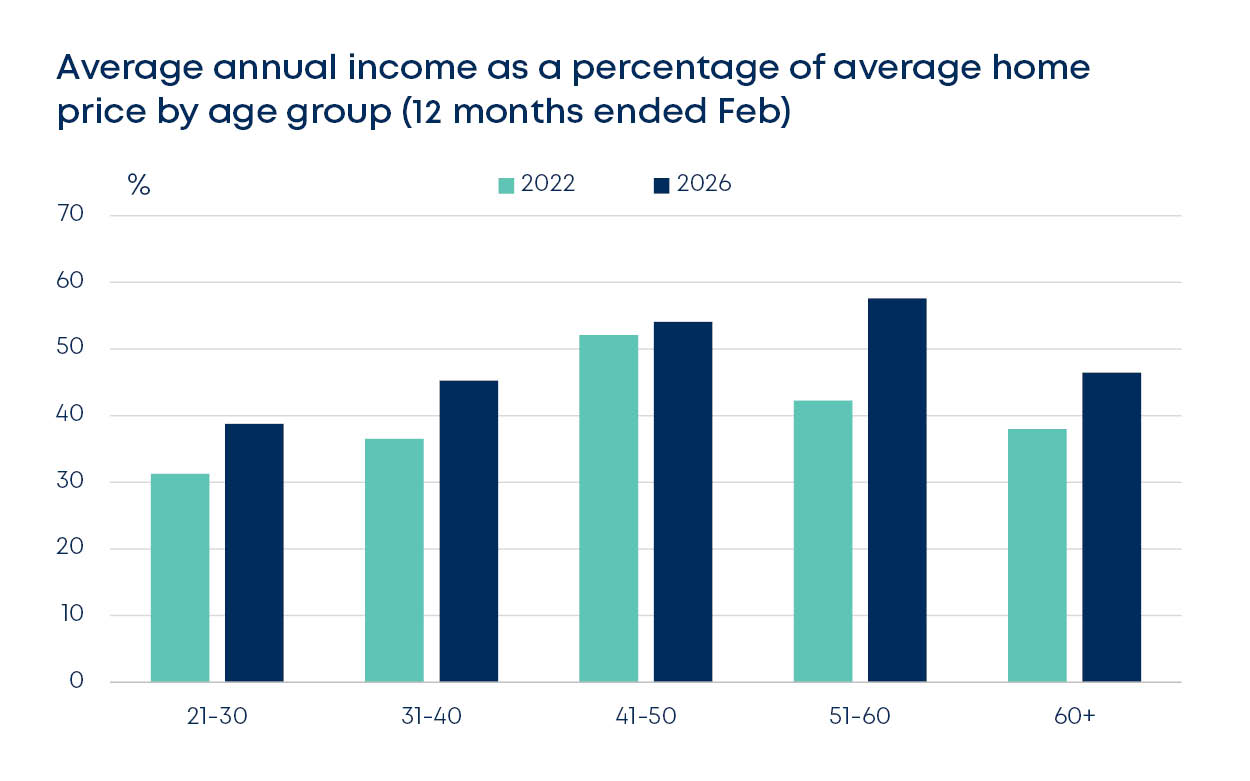

Affordability by Age: Older Buyers Gaining Ground

One of the more encouraging findings in the BetterBond data is the improvement in affordability ratios across age groups. Homebuyers aged 51 to 60 fared best over the past four years, with average annual income now equivalent to 58% of their average home purchase price — a 36% improvement since 2022. For all homebuyers, the average annual improvement in this affordability ratio is 5.1%, broadly in line with Stats SA’s reported average annual increase in formal-sector salaries of 4.3% over the same period.

Outlook: Cautiously Optimistic, Contingent on Ceasefire

The fundamentals underpinning South Africa’s property market are in better shape than at any point since 2022. Affordability is improving across age groups, approval rates are rising, and the national budget delivered tangible support for homeowners and buyers. The wildcard is entirely external: if hostilities in the Middle East subside and the rand stabilises, the Reserve Bank’s rate-cutting cycle could resume — and analysts believe this alone would push the BetterBond Index to new highs. For now, the market holds its breath.

Read the full report here.