MAIN IMAGE: Jee-A van der Linde, Economist of Oxford Economics

Staff Writer

South Africa has an economic risk score below, or better than, the average for both sub-Saharan Africa and emerging markets. The score has improved slightly over the past six months.

The main risk factors continue to be slow economic growth, stagnant fixed investment, weak manufactured goods exports, concerns over the sustainability of government spending, high government debt levels, governance issues at state-owned enterprises (SOEs) and uncertainties regarding, among other issues, ongoing appetite for land expropriation without compensation and unclear plans for National Health Insurance and the Basic Income Grant (BIG). Ongoing infighting and squabbling in the ANC also present a risk to policy.

This is the view of Jee-A van der Linde, Economist of Oxford Economics in a recent look at the economic outlook for South Africa over the next few months.

Van der Linde said the better-than-expected performance in Q1 2022 real GDP means that the economy has risen to pre-pandemic levels. The backward-looking data shows real GDP rose by a staggering 3.0% y-o-y in Q1. Although Q1 real GDP growth came in better than expected, and our 2022 economic growth forecast has been moved higher to 2.1%, the stagflation risks that we flagged during the previous forecast round remain firmly intact.

Business confidence deteriorated in Q2 after heavy flooding knocked business activity in April, and in the face of heightened global uncertainty. Manufacturers and new vehicle dealers experienced a sharp deterioration in sentiment, while building contractors turned more upbeat in Q2. Confidence among retailers and wholesalers was basically unchanged at relatively high levels.

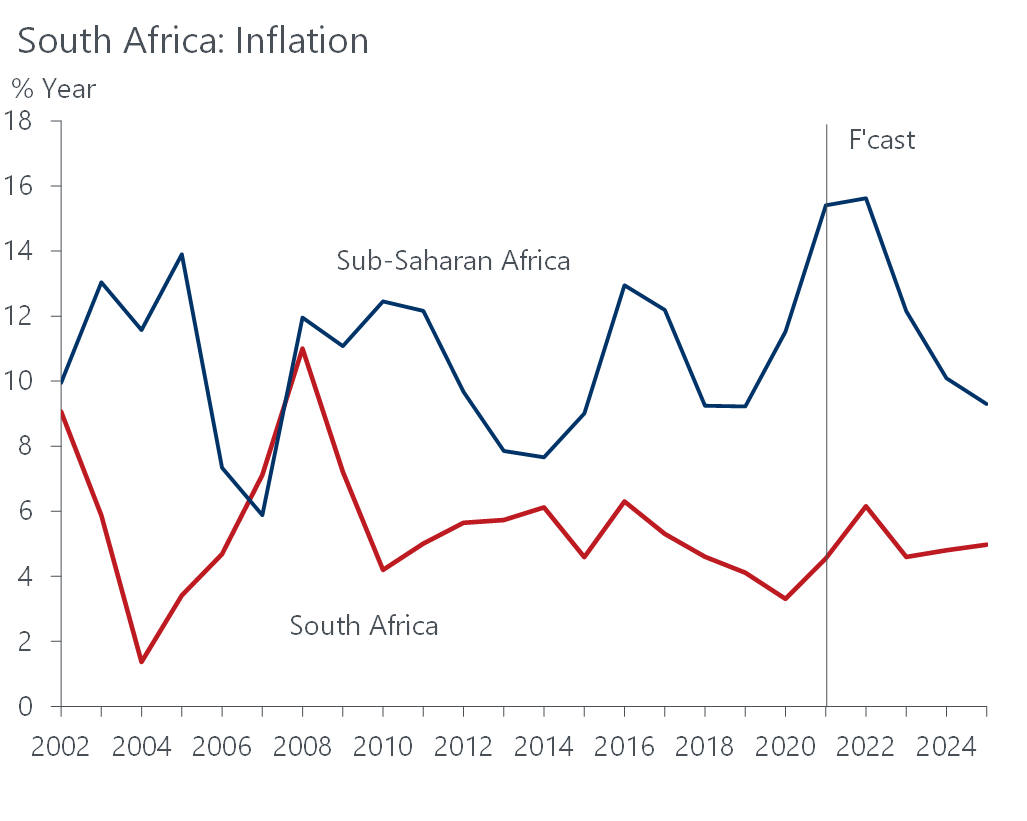

“We forecast the rand will end the year at R16.3/$ and to average around R16.1/$ in H2 2022 – despite ongoing Fed hawkishness until Q4. We believe that the rand will garner support from South African Reserve Bank (Sarb) hawkishness, and we now expect the repo rate to stand at 5.5% at end-2022, up from a previous forecast of 5.25%, with the balance of risks tilted towards a higher rate. This view assumes that inflation will remain above the upper limit of the inflation target well into H2, but base effects and an expected retreat in global commodity prices should direct inflation to 5.9% y-o-y by Q4 2022,” Van der Linde said.

He pointed out that South Africa’s inflation rate is now the highest it has been since early 2017. The CPI increased by 0.7% m-o-m in May, compared to 0.6% m-o-m in April. Goods inflation rose at a notably quicker pace in May, with food and non-alcoholic beverages, housing and utilities, transport, and miscellaneous goods and services contributing most to the annual increase.

According to Van der Linde the upside surprise in May also means that the Sarb will hike the repo rate by 50 bps during its upcoming policy meeting in July, with more frontloading likely to follow. We will likely revisit our forecast upon conclusion of the July Monetary Policy Committee (MPC) meeting. Meanwhile, the implied policy rate path according to the Sarb’s Quarterly Projection Model (QPM) points to gradual normalisation through to 2024.

“The potential growth for the year is seen at around 1.2%. After a protracted period of growth averaging roughly 1.0% because of structural problems such as policy uncertainty, poor labour relations and the low quality of education, we expect the pace of expansion to pick up, but only to an average of around 1.8% a year in 2025-29.

“The key long-term issues are:

- Implementation of economic reforms:The government’s appetite for reforms that challenge vested interests has been feeble in recent years and Pres Ramaphosa’s explicit commitment to reform has not translated into action. The urgent need for fresh policy thinking means there is a real opportunity to rejuvenate the policy agenda.

- Under-utilisation of resources:Unemployment is set to remain exceptionally high. South Africa has a history of low investment. However, if workers were to be brought into the formal sector more rapidly and if investment could be stimulated, long-term growth prospects would improve considerably.

- Legacy of state capture:Corruption flourished under former Pres Jacob Zuma’s tenure, and state capture had become entrenched in South Africa, crippling the economy. Misspending, as opposed to just excessive expenditure, and poor revenue growth have contributed to the precarious financial position, which leaves very little room for fiscal stimulus.

“The economy is stuck in a low growth trap. South Africa’s economic outlook points to some near-term growth but the medium-term prospects are dull. Decisive action on the policy front is needed to serve as a driver of growth. State capture has seen the economy’s bottom fall out, and widespread inefficiency at a government level means that increased private sector involvement is essential. South Africa’s young and growing population does not just require new schools to be built; it desperately needs jobs and, importantly, the appropriate knowledge and skills. Even with the finest business environment and a strong growing economy, job creation will take time,” Van der Linde concluded.