Partner content

South Africa’s residential property market is maintaining its recovery trajectory, but estate agents should note significant shifts in lending conditions that could affect buyer behaviour in the months ahead.

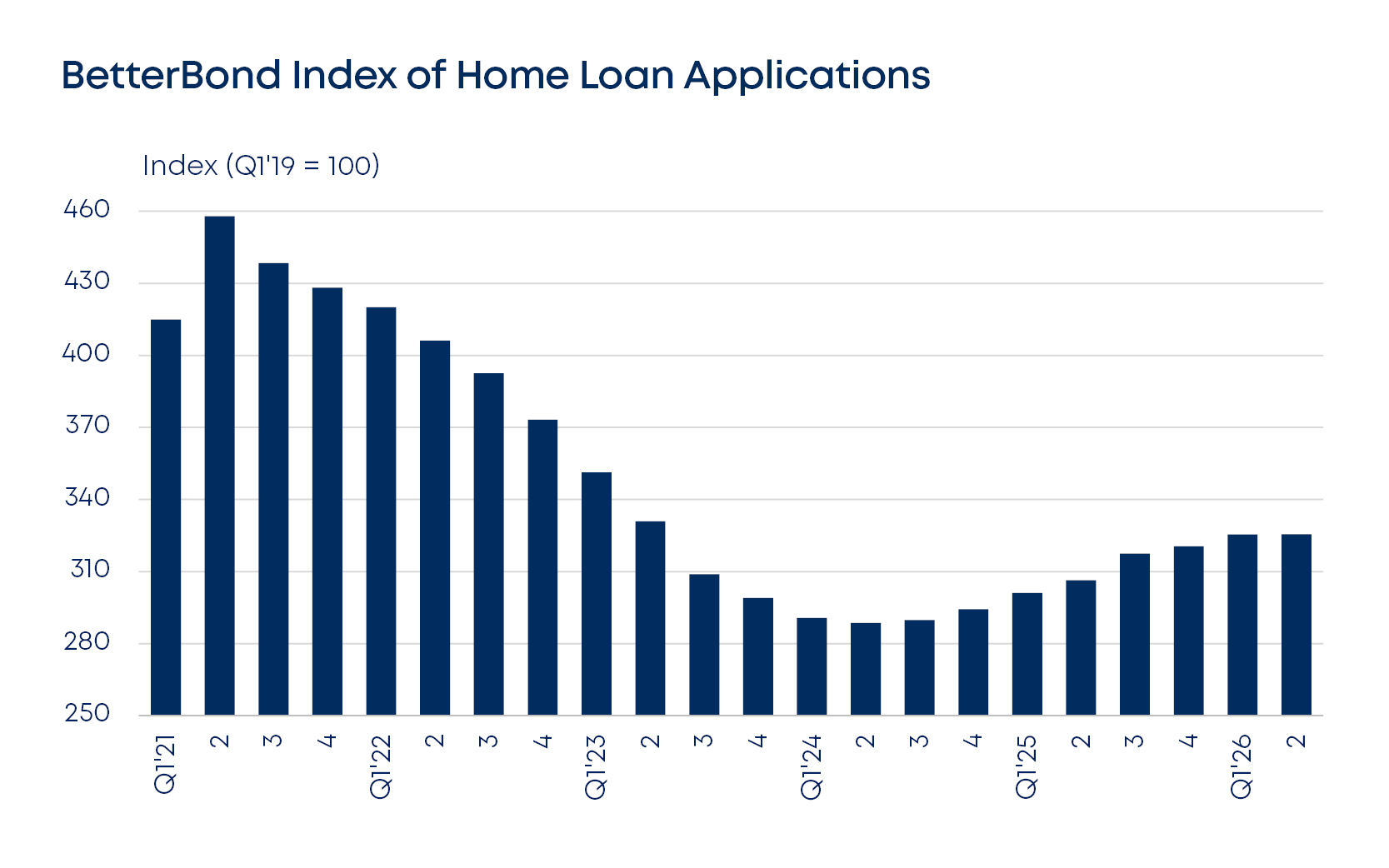

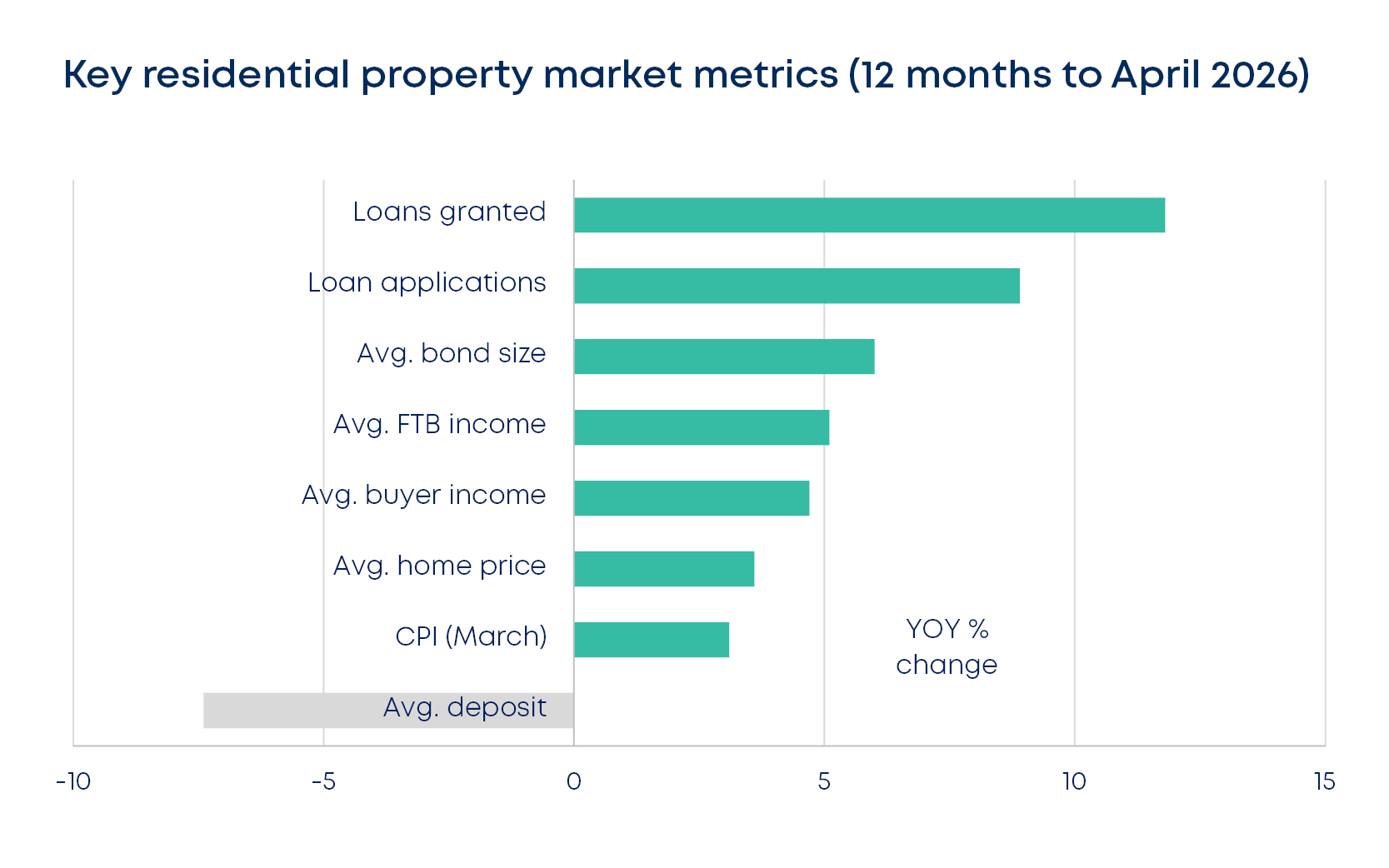

Home loan applications grew 6.2% year on year in April, continuing the upward trend that began when the rate-cutting cycle started in Q3 2024. Since then, the BetterBond Index of Home Loan Applications has improved by 12.3%, and home loans granted are up 11.8% year-on-year. Average home prices have also reached new highs, with the overall market breaching R1.7 million in April and first-time buyers (FTBs) hitting a record R1.4 million. FTB prices recorded year-on-year growth of 10.3%, while repeat buyers saw an even stronger 19.9% increase.

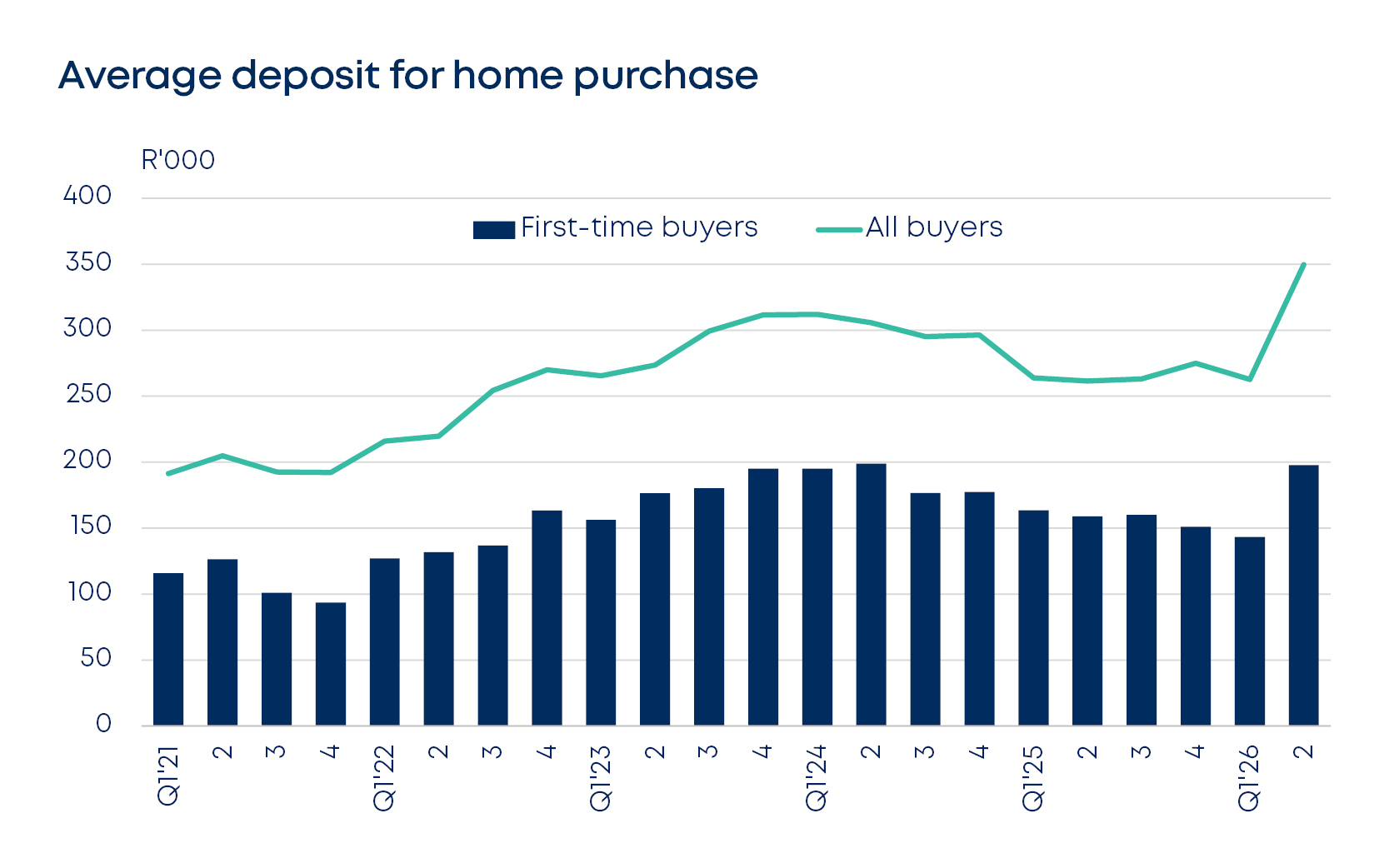

The big story for agents to watch, however, is deposits. After eight consecutive quarters of declining deposit requirements, banks sharply reversed course in April, with a 33% quarter-on-quarter increase for all buyers. FTBs have been hit hardest: the average deposit requirement jumped from R143,000 to R198,000 in a single month, taking it back to levels last seen in Q2 2024. FTBs are now expected to put down, on average, the equivalent of 38% of a home’s purchase price. This is a material shift that agents will need to communicate carefully to buyers who may have budgeted based on earlier, more favourable lending conditions.

The deposit increase appears to reflect growing caution among banks amid potential inflationary pressures, driven largely by elevated global fuel prices. Oil remained above $100 per barrel in late April and early May due to the effective closure of the Strait of Hormuz, and there is concern that if fuel prices feed through into broader inflation, the South African Reserve Bank could pause or end the rate-cutting cycle. Any stalling of rate cuts would dampen the momentum the market has been building.

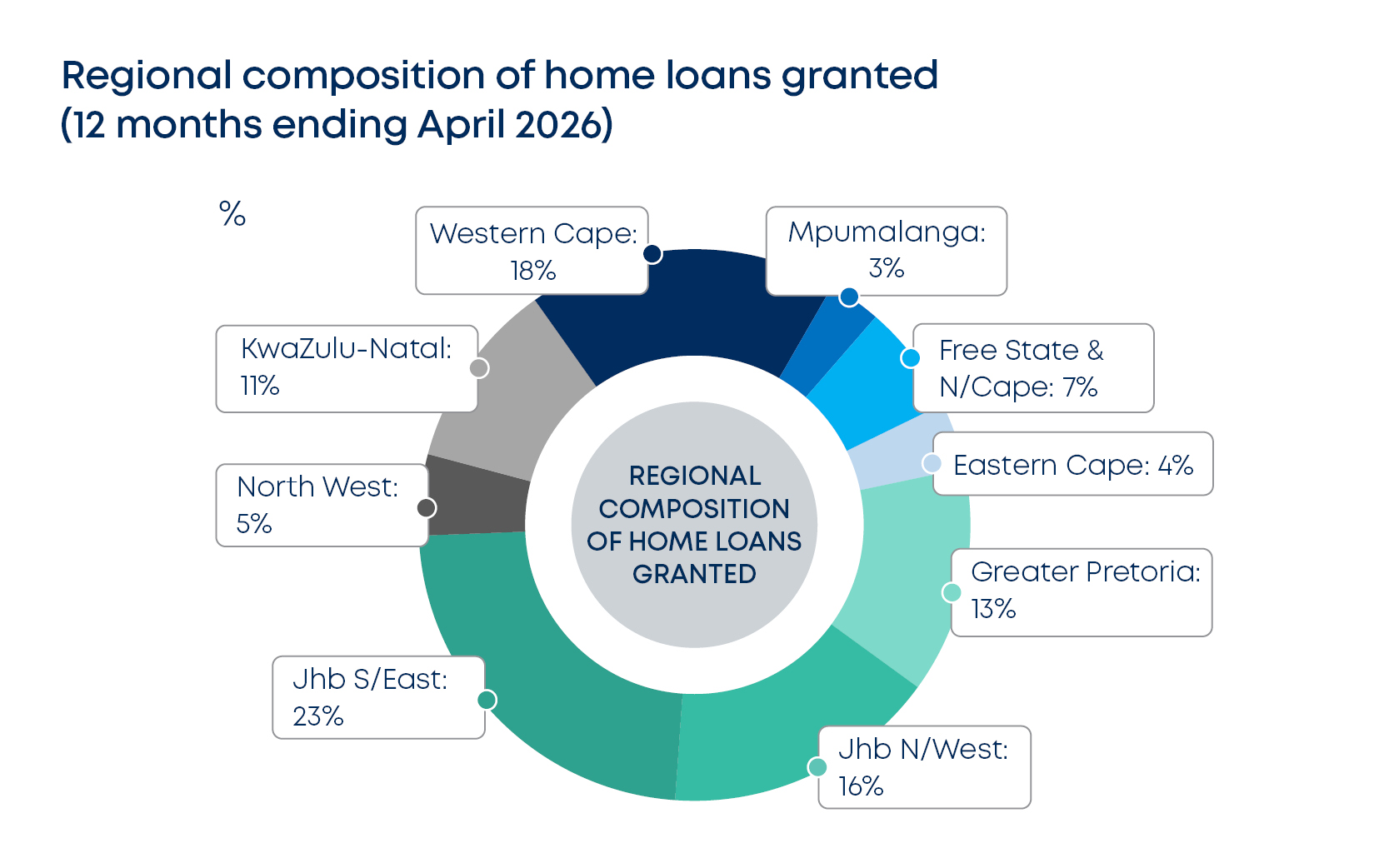

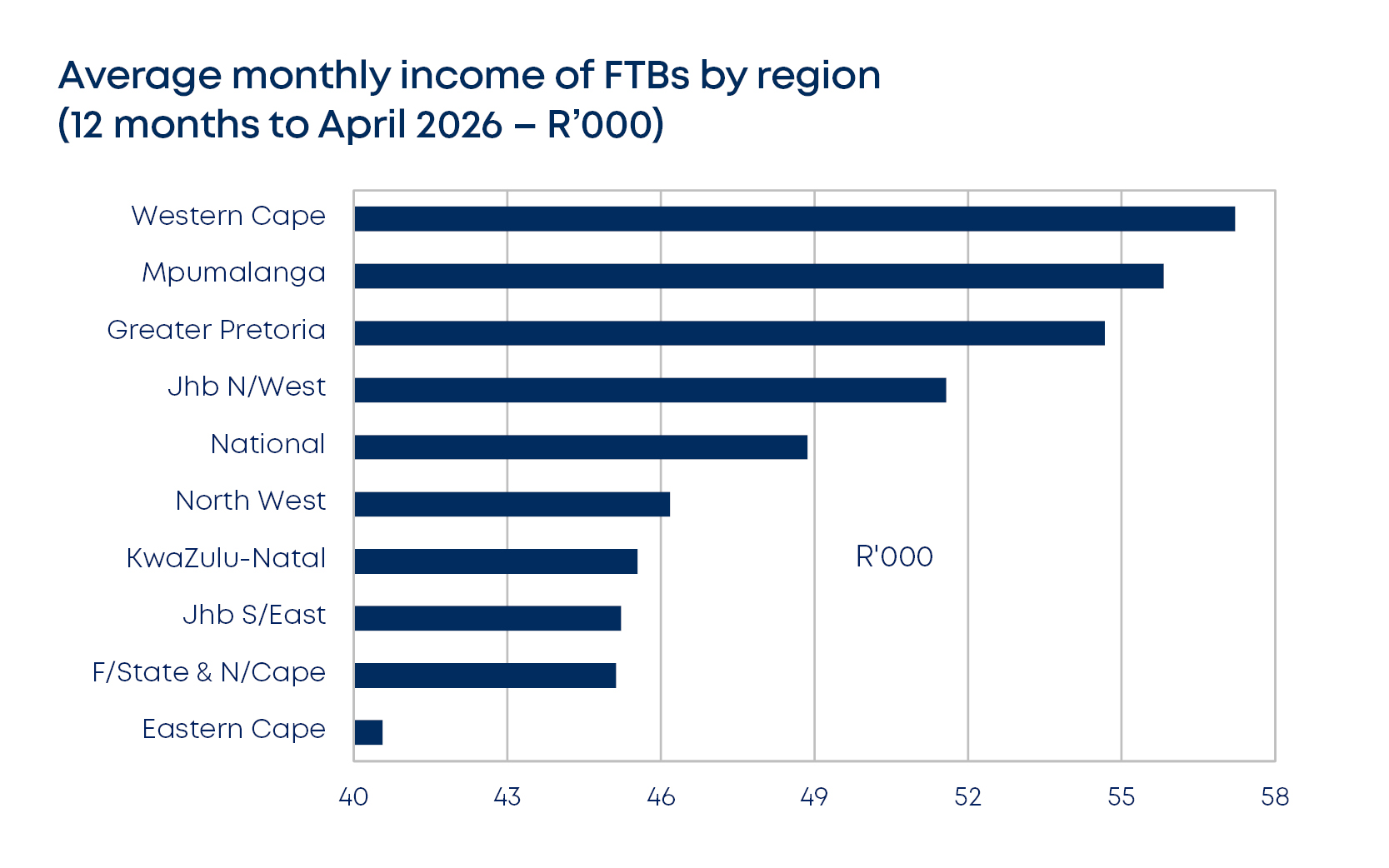

Regionally, Johannesburg’s South-Eastern suburbs continue to lead the country in home loans granted, holding 23.3% of the national share and recording the highest growth among regions over the past year, at 28.6%. The Western Cape is firmly in second place with a 19.3% share and has also recorded the highest growth in average bond values. FTB incomes in the Western Cape now lead the country, averaging R57,200 per month, up 9.7% year on year, reflecting strong economic activity in the province. Greater Pretoria holds the second-highest average bond value at R1.5 million.

On the construction cost side, agents advising clients on new builds should note that cement costs rose 13.7% year on year, with electrical cable and equipment also seeing double-digit increases. Overall construction input prices rose 4.3%, outpacing the Consumer Price Index, which means replacing or building property remains comparatively expensive and supports the value of existing stock.

The broader economic picture offers some cause for optimism. South Africa’s cumulative trade surplus for Q1 2026 trebled to R77 billion, household incomes are rising ahead of inflation, and China’s new zero-tariff policy for African goods exporters, effective from 1 May, could provide further economic stimulus. For now, the fundamentals support continued market activity, but the deposit shift is a real and immediate pressure point that agents and their clients need to factor into purchase planning.