First National Bank

The latest FNB General Household Survey (GHS) points to structural shifts in South Africa’s housing tenure, with demand increasingly tilting toward rental rather than ownership. This reflects the interaction of robust household formation, weaker affordability, and more constrained mortgage access, alongside persistent urbanisation.

However, there is likely continued divergence between those who can afford to and prefer to own property, and households with financial constraints. To focus on underlying trends, the analysis compares 2019 with 2025, thereby avoiding distortions associated with the 2020 Covid-19 disruption. This note explores the implications of these trends for property markets.

Population dynamics: Strong household formation and deepening urban concentration

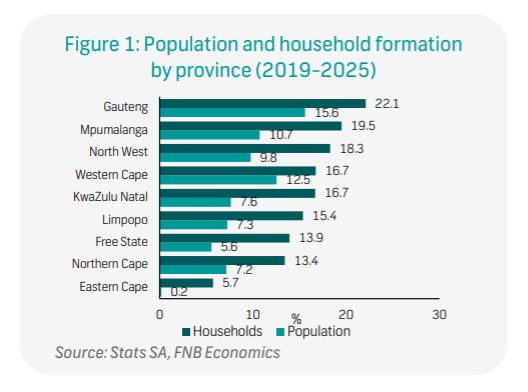

Between 2019 and 2025, household formation remained strong, rising by 17.2% (from 17.2 million to 20.1 million) and outpacing population growth of 9.7%. This implies a continued decline in the average household size, increasing the number of housing units required per capita, and representing a structural uplift in underlying housing demand, despite a weak macroeconomic backdrop. Provincially, Gauteng leads, with its household base expanding by 22.1%. KwaZulu-Natal and the Western Cape also recorded above-average growth (16.7% each), reinforcing the concentration of population and economic activity in key urban areas.

At the metro level, this concentration has intensified. Gauteng metros remain the primary drivers of growth, outpacing smaller urban centres and reinforcing the dominance of large nodes (Figure 2). This reflects the continued pull of labour market opportunities and access to services, suggesting urbanisation remains structurally embedded despite pandemic disruptions. The post-2021 recovery has largely reinstated pre-existing migration patterns, with implications for both housing demand and commercial activity.

Housing tenure: Constrained entry into ownership?

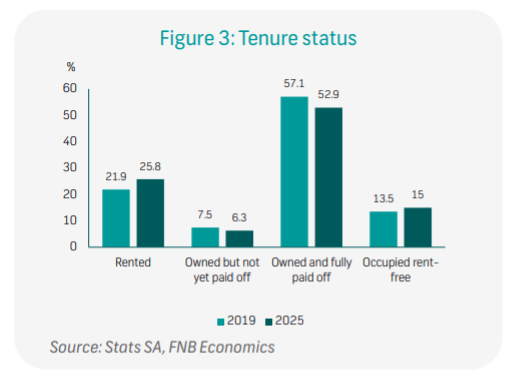

The most significant change is in housing tenure. The share of renting households increased from 21.9% in 2019 to 25.8% in 2025, equivalent to roughly 1.4 million additional renter households. This marks a clear re-weighting of the housing market toward rental demand. Mortgage-linked ownership declined modestly from 7.5% to 6.3%, while fully-paid ownership also fell in share terms, from 57% to 53%.

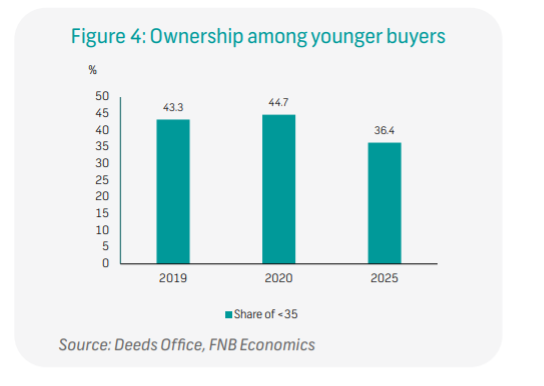

These shifts reflect more than cyclical dynamics. While ultra-low interest rates between 2020 and 2021 initially supported ownership, particularly among younger buyers, the subsequent tightening in financial conditions imposed a material constraint. Higher borrowing costs and weak real income growth reduced affordability, while tighter credit conditions limited mortgage access. As a result, the transition from renting to ownership weakened, with rental demand reflecting both reduced entry into ownership and some fallback from ownership, reinforcing a more persistent shift in tenure dynamics. Supporting this, Deeds data shows that, outside the brief 2020-2021 period, the <35-year-old age group has experienced a structural decline in ownership levels.

However, female ownership levels continue to trend upward, pointing to a gradual shift in the composition of homeowners. In addition, our Estate Agents survey has consistently shown that once households transition to ownership, they are more likely to transition within the ownership market (e.g. trading across price segments), rather than reverting to rental. Together, this suggests that the tenure shift is being driven primarily by weaker entry into ownership, rather than significant exist from ownership.

Implications for the residential property market

Overall, the housing market is becoming increasingly rental-led, particularly in metros, driven by demographic and affordability dynamics. Strong household formation combined with affordability pressures is reinforcing demand for build-to-rent, sectional title rentals, and affordable multifamily housing. Weaker mortgage-backed ownership suggests that unlocking the entry-level segment will require more innovative financing structures and sustainably easier credit conditions.