BetterBond

South Africa’s residential property market is showing early signs of recovery, but geopolitical uncertainty continues to temper the pace, according to BetterBond’s April 2026 Property Brief.

“Improving fundamentals are supporting renewed activity in the property market, but elevated geopolitical risk continues to influence confidence, interest rates and the pace of recovery,” says Stephan Potgieter, CEO of BetterHome Group Mortgage Origination and BetterBond.

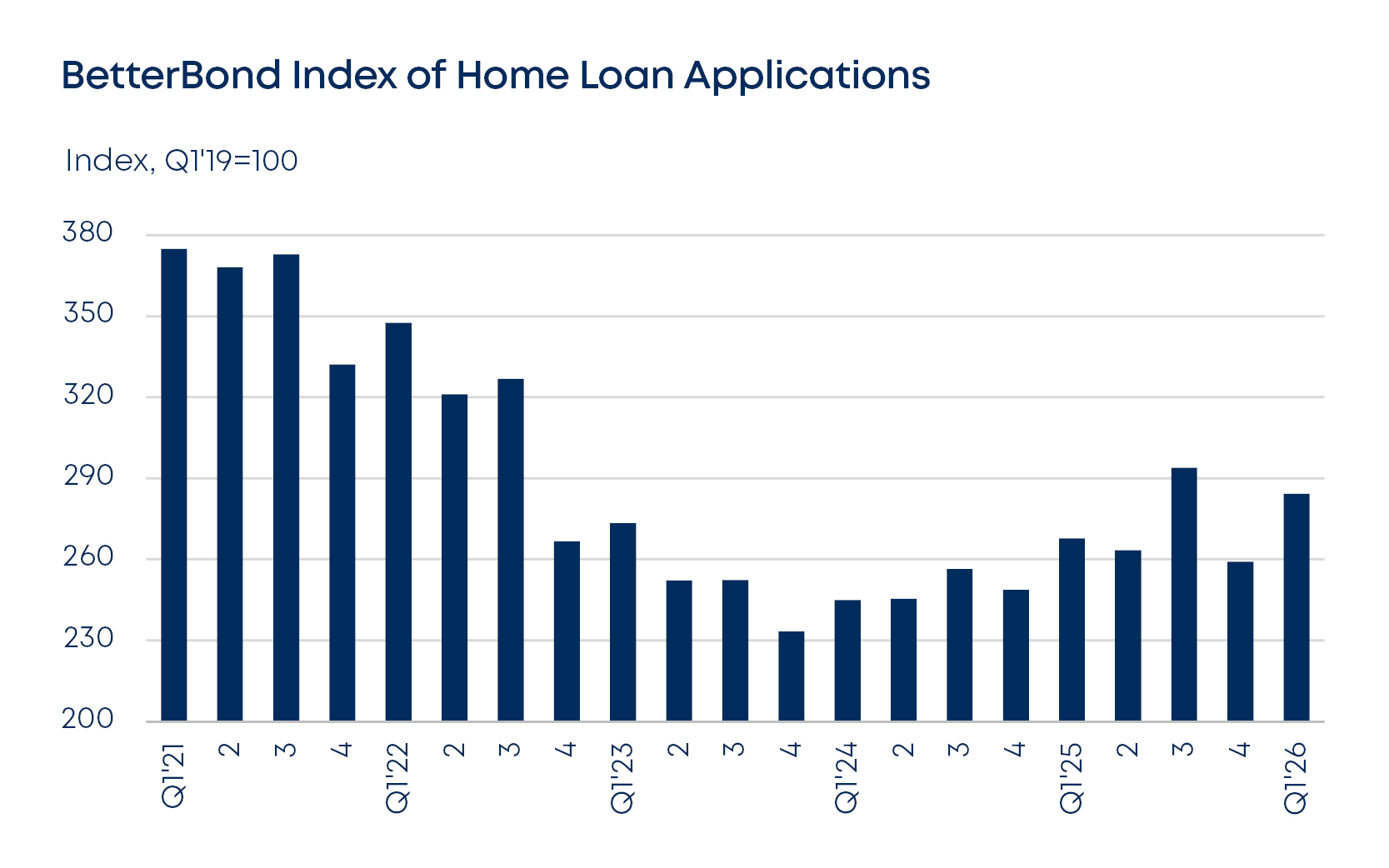

Home loan applications on the rise

Home loan applications rose 9.7% quarter-on-quarter during Q1 2026, building on a recovery of 21.8% since the low point of Q4 2023, when interest rates hit a 15-year high. Year-on-year, applications are up 6.1%, consolidating a two-year recovery rate of 16%.

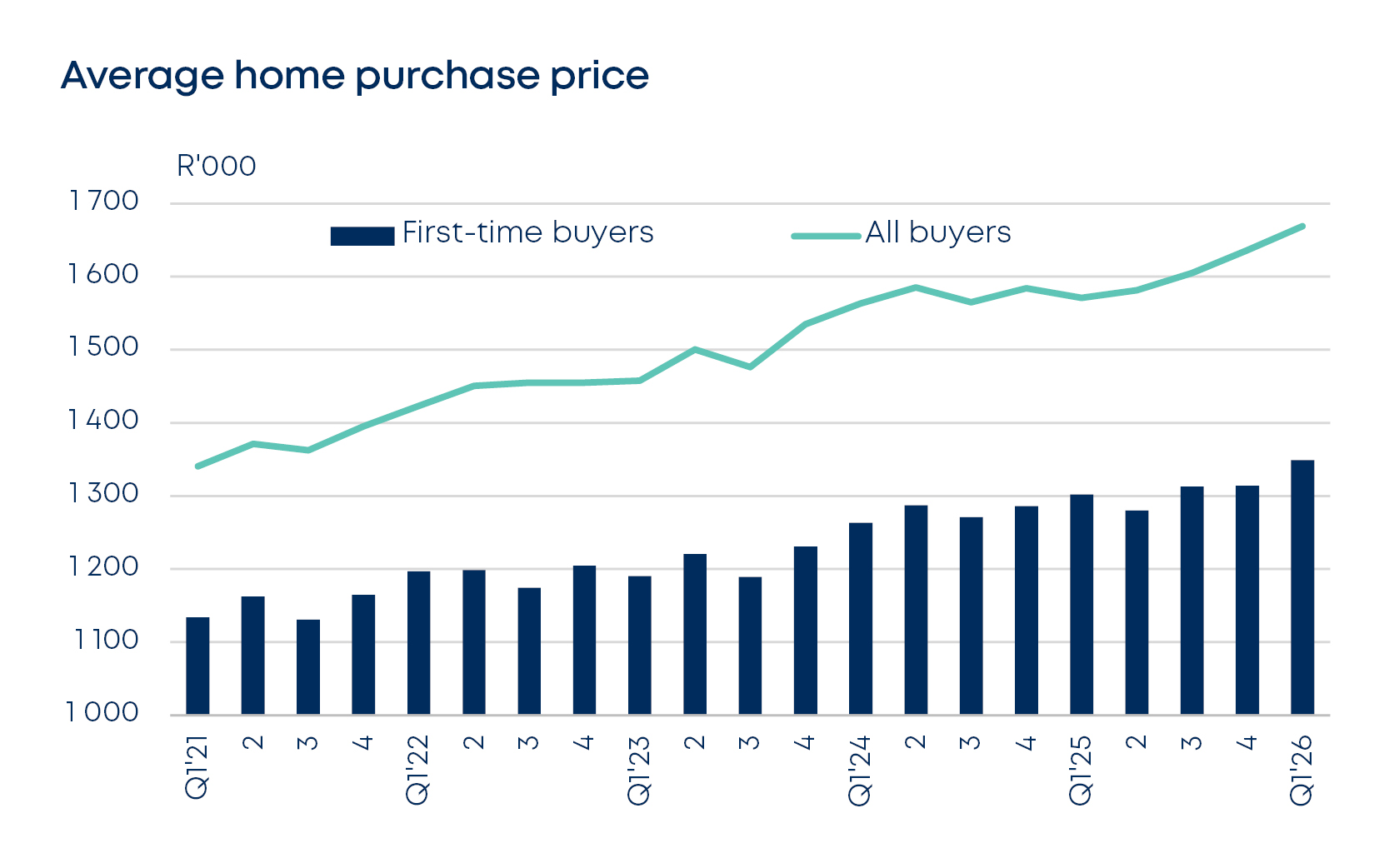

Record house prices, improving affordability

Average house prices reached new record highs during Q1 2026, with the overall buyer average climbing to R1.67 million and the first-time buyer (FTB) average reaching R1.35 million. In real terms, prices rose 3.2% year-on-year across all buyers, with FTBs recording growth of 3.6% and repeat buyers 5.3%.

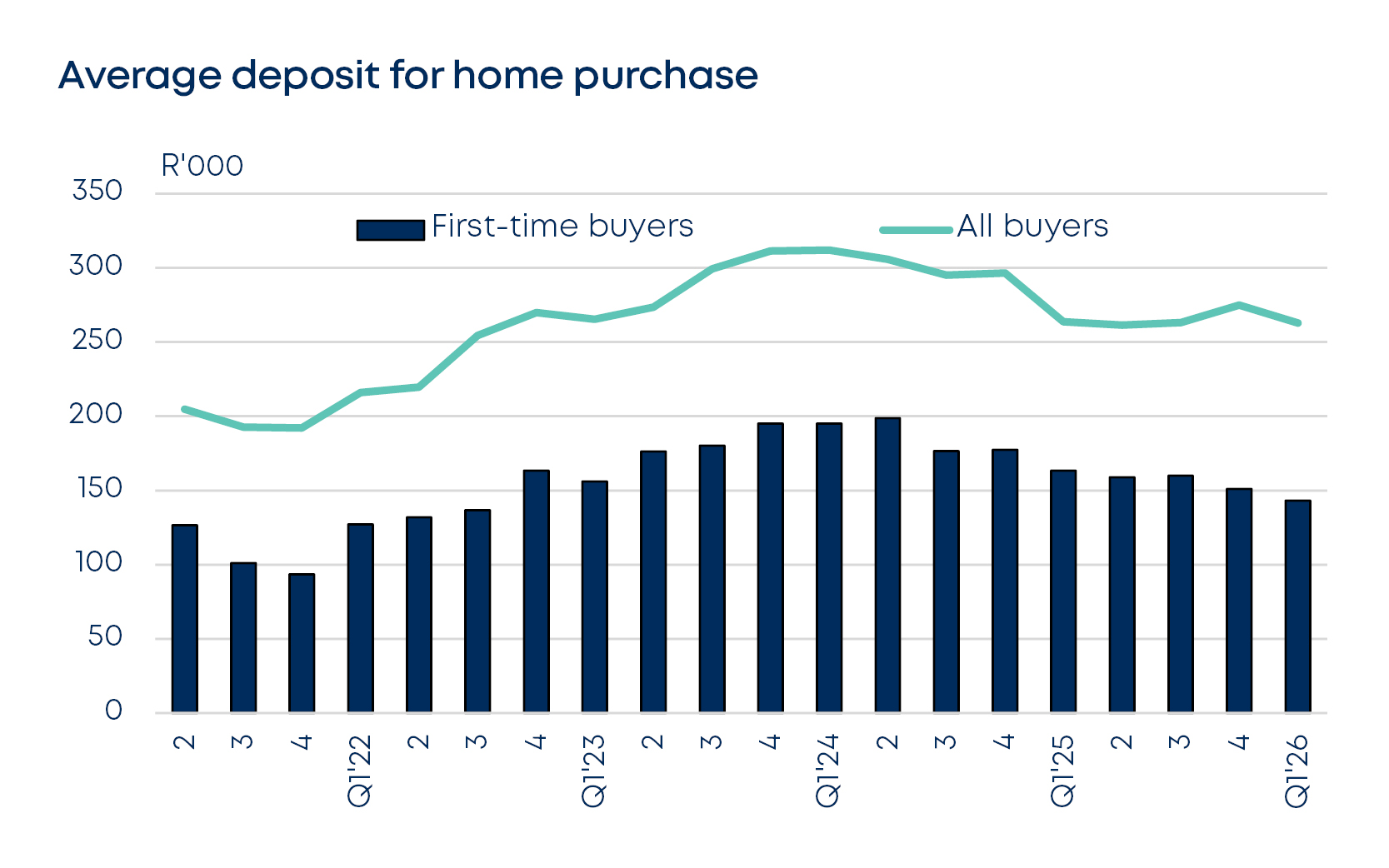

Conditions for first-time buyers have improved further, with the average deposit requirement declining by 26.6% since Q1 2024. The FTB share of home loans has climbed from 35.4% in 2023 to 38%, driven by lower interest rates. The prime lending rate currently stands at 10.25%, where it has been held as the rate-cutting cycle that began in September 2024 has stalled in the wake of the Middle East conflict.

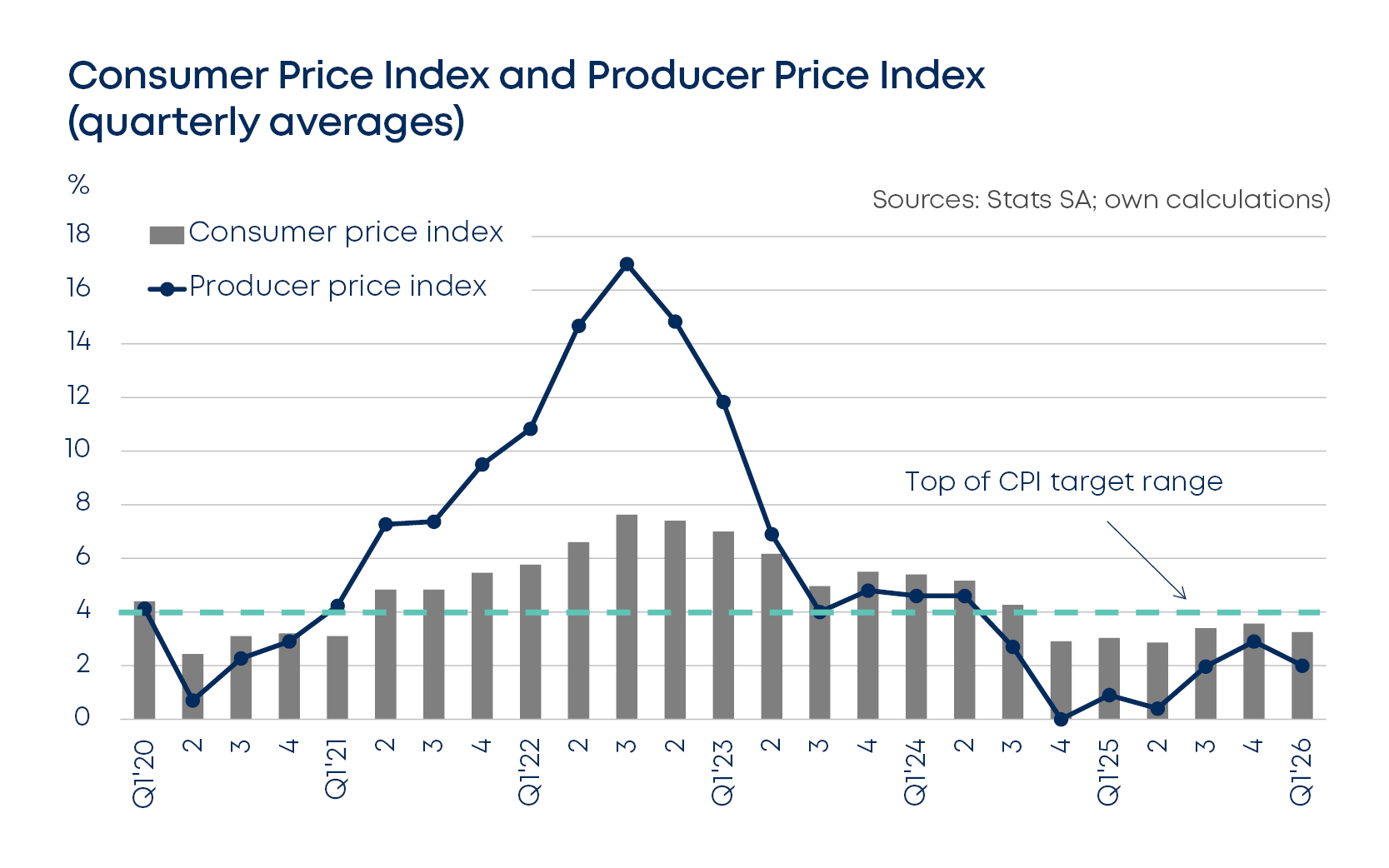

The geopolitical wildcard

Geopolitical risk is a central theme in this month’s brief. The ongoing Gulf war has driven oil and fuel price increases, placed upward pressure on inflation, and contributed to the Monetary Policy Committee’s decision to keep the repo rate on hold. The brief draws on the Geopolitical Risk (GPR) index, developed by researchers Caldara and Iacoviello, to contextualise the impact of global instability on property markets. A 2026 study published by the Multidisciplinary Publications Institute confirms that elevated geopolitical tensions have increased volatility and negatively affected property returns across BRICS countries.

Domestic fundamentals remain constructive

Despite this, several domestic indicators remain positive. Inflation has continued to decline, with both the Consumer Price Index and Producer Price Index trending downward.

South Africa’s trade account recorded a cumulative surplus of R45.4 billion in the first two months of 2026, largely on the back of a 39% year-on-year increase in precious metal export values. Average real incomes for homebuyers have grown at 5.4% annually over the past four years, significantly outpacing the economy-wide average of 0.3%.

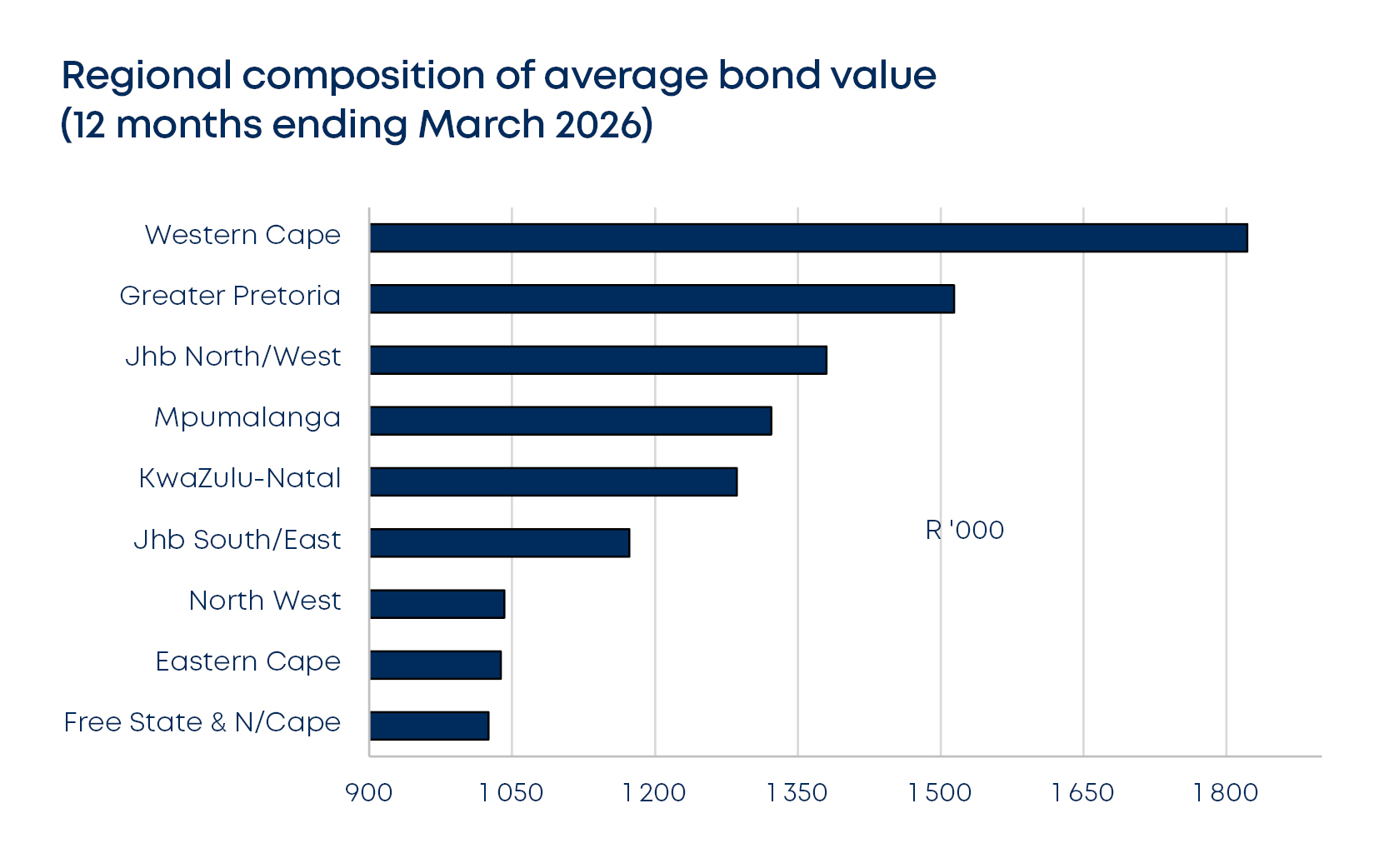

Western Cape leads on value, Pretoria closes the gap

Regionally, the Western Cape leads on average bond value at R1.82 million, with Greater Pretoria second at R1.4 million. Cape Town recorded an 18.1% increase in average home loan value over the past two years, compared with an average of 4.4% across Johannesburg’s suburbs. Every region tracked by BetterBond has now broken through the R1 million average bond value threshold.

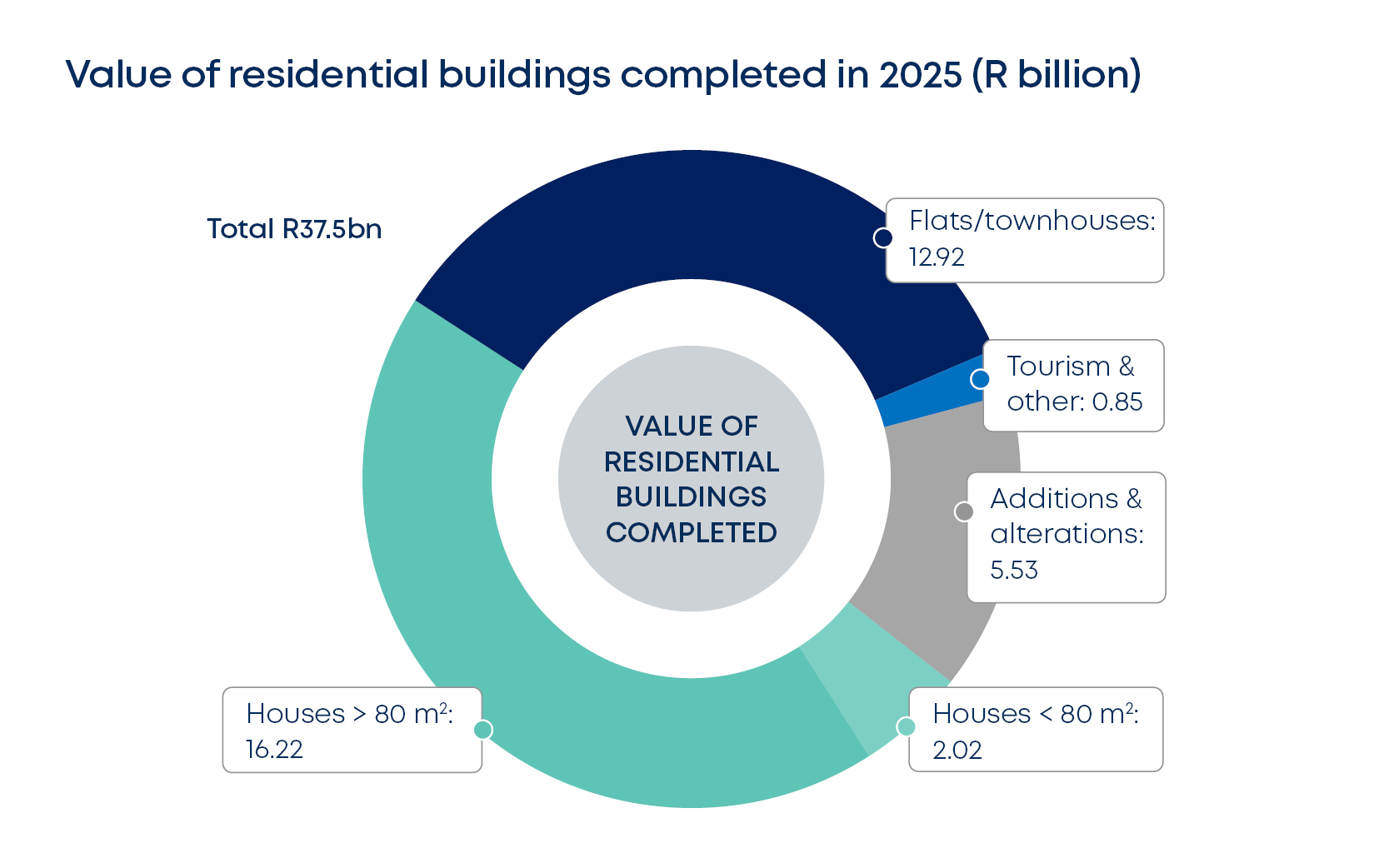

Smaller units, stronger numbers

In the residential building sector, 2025 saw a marked shift toward smaller units. New flats and townhouses recorded growth of 27%, representing 34.4% of the total value of completed residential buildings. Gauteng, the Western Cape and KwaZulu-Natal together accounted for 88% of new residential completions nationally.

What to watch

While the outlook for recovery is broadly positive, a swift resolution to Middle East hostilities would be the most significant single catalyst for resuming the interest rate cutting cycle and accelerating momentum in the housing market.